Cash is king in retail.

Financial challenges continue to be top of mind for small businesses, with nearly half (48%) saying they feel the pressure of increased operating expenses. If you don’t have cash to pay for inventory, expenses, or unforeseen costs, it can be a struggle to thrive.

A merchant cash advance is one option for dealing with a cash crunch. It offers low-cost business financing that can help your business clear financial obstacles. Learn how it works and how you can get one to inject capital into your business and grow.

What is a merchant cash advance (MCA)?

A merchant cash advance (MCA), as the name implies, is a business funding option that “advances” your business cash. It is a type of working capital financing that enables you to obtain funding quickly for expenses such as salaries, rent, and inventory costs. You then repay the amount based on a percentage of sales, plus a small fee. It’s best for small businesses that accept card payments from their customers. You only repay the advance as more cash flows into your business.

How does a merchant cash advance work?

Merchant cash advances are different from traditional business loans. They are unsecured, which means you don’t need any assets—like inventory or property— to use as collateral to get funding. With an MCA, the lender gives you a lump sum of money that you repay through sales.

Here’s how the process works:

1. A lender looks at your sales, generally the average value of card sales.

2. They offer you a lump sum of cash.

3. You accept the advance.

4. You pay the lender a percentage of card sales.

You can often choose daily, weekly, or sometimes, monthly repayment plans. However, since repayment is based on sales, a business with higher credit card sales can repay the cash advance quicker. The lender deducts a percentage of sales (typically at least 10%).

The flexibility of cash advances can work well for businesses with seasonal highs and lows.

Each lender has different eligibility requirements for getting a merchant cash advance. For example, to use Shopify Capital, you need:

1. A Shopify seller’s account and business bank account

2. A store located in the US, Canada, Australia or the UK

3. A business assessed as “low risk”

4. To use Shopify Payments or a compatible third-party payment provider

5. To meet a certain level of sales regularly

Overall, a merchant cash advance is an easy and fast way to get business funding if you need it.

I really love the flexibility of the repayment system of Shopify Capital. On busy days I repay more, and on slower days I repay less.

Merchant cash advances vs. other financing options

Taking a personal inventory of your business needs is a crucial step in deciding the best financing option. You can accomplish this by asking yourself a few key questions, including: How quickly is the money needed? Are there any owned assets that can be used as collateral? Does the business experience seasonal lulls? The answers can provide helpful guidance about which option is the best fit when considering these alternatives to a merchant cash advance:

1. Traditional bank loans

Traditional bank loans have a fixed payment schedule (frequently monthly) and payment amount that the business pays. Merchant cash advances are not considered loans, repayment amounts are more flexible, since they’re based on percentage of business sales, and are typically withdrawn automatically from your account.

2. SBA loans

SBA loans are backed by the Small Business Administration and offer different types of loans, depending on your business needs, such as:

- Disaster assistance. These loans focus on disaster relief and have specific criteria for businesses impacted by natural disasters such as floods, earthquakes, and wildfires. Applications can take two to three weeks to process, and repayment terms can extend up to 30 years.

- Small microloans. Microloans are up to $50,000 and for underrepresented businesses, including startups and entrepreneurs. Repayment terms are up to six years and may require collateral.

- 7(a) loans. SBA 7(a) loans offer longer repayment periods and lower interest rates, with specific criteria for eligibility and detailed repayment terms. A standard loan can take five to 10 days for processing.

Meanwhile, with a merchant cash advance, your business may receive funding in a few days. Repayments can start as quickly as on a daily or weekly basis since based on sales. And, no collateral is required.

3. Credit cards

A business credit card offers a way to quickly finance business expenses, and can be a resource when bootstrapping. You can expect a predetermined spending limit and the ability to separate personal and business expenses—although you may face a high interest rate and can be held personally liable if you default on the debt.

Merchant cash advances don’t offer the credit card perks such as discounts on business-related expenses such as shipping or cash-back offers.

4. Business lines of credit

Business lines of credit (LOC) allow you to take draws against a loan amount and make interest-only repayments. Depending on the type of lines of credit, you may—or may not—be required to have collateral.

Merchant cash advances don’t require good credit; LOCs typically do.

Advantages and disadvantages of a merchant cash advance

Unlike some alternative financing options, merchant cash advances offer a quick way to get business funding. You can expect application approval within 24 to 72 hours (and MCAs tend to have high approval rates).

Among the advantages and disadvantages of getting a merchant cash advance:

Advantages of a merchant cash advance

- Flexible payment options. Since repayment is based on sales, you can pay what you can afford—because when sales drop, so does your payment amount.

- Easy repayment. The MCA lender takes its repayments from total sales, automatically deducting the amount from your business account.

- Easy access. You can secure a cash advance without collateral, and with little, no, or poor credit.

- Fast funding. Funding happens quickly, typically within days.

- Low risk. The loan pays itself off since adjusted to sales; no separate loan payments are necessary.

- Transparent. No hidden fees; costs are set at start through the lender’s agreement.

Disadvantages of a merchant cash advance

- Expensive. The cost may be higher than a standard loan. When considering its factor rate as an interest rate, you could be paying between 20% and 50% on top of the advance amount.

- Frequent payments. You typically can expect to repay the MCA on a daily or weekly basis, versus making monthly loan payments.

- Short-term funding. MCAs, with their high costs, are designed for short-term cash relief.

- Limited to card payments. MCAs are best for businesses that only accept credit and debit card transactions. Lenders choose whether or not to give an MCA based on card turnover, or how many card payments are accepted over a period of time. If you get a lot of cash payments, a lender could deny your MCA request.

Merchant cash advance terms and features

These are common terms and features associated with merchant cash advances:

Principal

The principal refers to the amount you borrow and must repay. When you take out an MCA, the size of the advance is the principal. As you make payments on the MCA, a portion of those payments reduces your principal and the rest pays the fee determined by your factor rate.

Factor rate

The factor rate determines how much in total you pay for the MCA. For example, if your MCA amount is $10,000 and your factor rate is 1.2, your total payback is $12,000 (10,000 x 1.2).

Factor rates vary by lender and business, but can range between 1.1 and 1.5.

Payment period and frequency

The payment period is the timeframe you have to pay back the advance. MCAs have a payment period of anywhere from three months to 24 months.

Frequency is how often you pay back the MCA. Most business owners make daily or weekly payments.

Percentage deduction of credit card sales

You repay a cash advance by giving a percentage dedication of credit card sales. The number varies by lender, but can range from 5% to 20% of sales.

How to get a merchant cash advance

1. Research providers

2. Fill out application forms

3. Decide which deal is best for your business

Getting a merchant cash advance is simple. Many providers offer an easy online application with quick approval times. Applying for an MCA can take a few minutes. Even businesses with a short history and poor to average credit can be eligible for a merchant cash advance.

Once you decide an MCA is right for you, find a provider that offers the best deal. If you have a Shopify store and use Shopify Payments, you can check your eligibility with Shopify Capital.

If you choose another provider, be prepared to submit the following in your application:

- Company structure

- Business income

- Estimated income growth

- Bank account statements

- Credit card processing statements

💡 PRO TIP: Avoid lengthy application processes, paperwork, and credit checks, and get funding within days with Shopify Capital. Get the funds you need to open a retail store, invest in staff, inventory, and marketing, and pay it off as a flexible percentage of your sales.

Uses for merchant cash advances

Common ways you can use an MCA include:

1. Purchasing inventory

Keeping products in stock is critical to retail growth. Sometimes, retailers are limited to how much they can sell because they don’t have the money to buy inventory.

With an MCA, you can stock up on inventory, get ready for seasonal sales, or take advantage of bulk discounts. For example, if you want to prepare for the Black Friday Cyber Monday (BFCM) season and you’re running low on capital, you can get an MCA to stock up ahead of time.

💡 PRO TIP: Shopify POS comes with tools to help you control and manage your inventory across multiple store locations, your online store, and warehouse. Forecast demand, set low-stock alerts, create purchase orders, know which items are selling or sitting on shelves, count inventory, and more.

2. Purchasing equipment

Having sufficient capital allows you to invest in new equipment, which can improve efficiencies and help you sell more. For example, if you need retail signage, or mannequins and shelving to showcase your clothes, you can get funding fast from an MCA.

3. Marketing

Whether it’s Google Ads or building a social media presence, you can use money from your MCA to support your marketing efforts.

You can invest in:

- A higher ad budget to get the word out and convert more customers

- Refreshing your brand identity with new packaging and photos

- Running a contest to get more social media engagement

- Partnering with an influencer to tap into new audiences

💡 PRO TIP: You can set up, track, and manage local inventory listings and Smart Shopping Campaigns from the Google & YouTube app for Shopify. Get all the perks of marketing your business on Google without jumping between accounts.

4. Cash flow relief

Managing cash flow is a frequent problem for retailers. One study found that 45% of US small businesses experienced cash flow challenges that impacted their ability to pay themselves, and leaving some unable to pay bills. Such financial pressures led 85% to make cash flow management a priority.

Since the approval process for MCAs is quick, you can get cash into your business for:

- Wages

- Supplies

- Materials

- Distribution

- Events

💡 PRO TIP: Take control of your cash flow with Shopify Payments. Get a complete view of your business finances, know when to expect payouts, track in-store and online sales and payments, and manage your money where you run your business.

5. Unforeseen costs

Additional funding can also help cover unforeseen expenses. For example, you can use a cash advance to pay for equipment maintenance or upgrades, cover professional service costs, or take care of any other hidden costs that may arise.

3 examples of merchant cash advances

Here are a few potential options for securing a merchant cash advance:

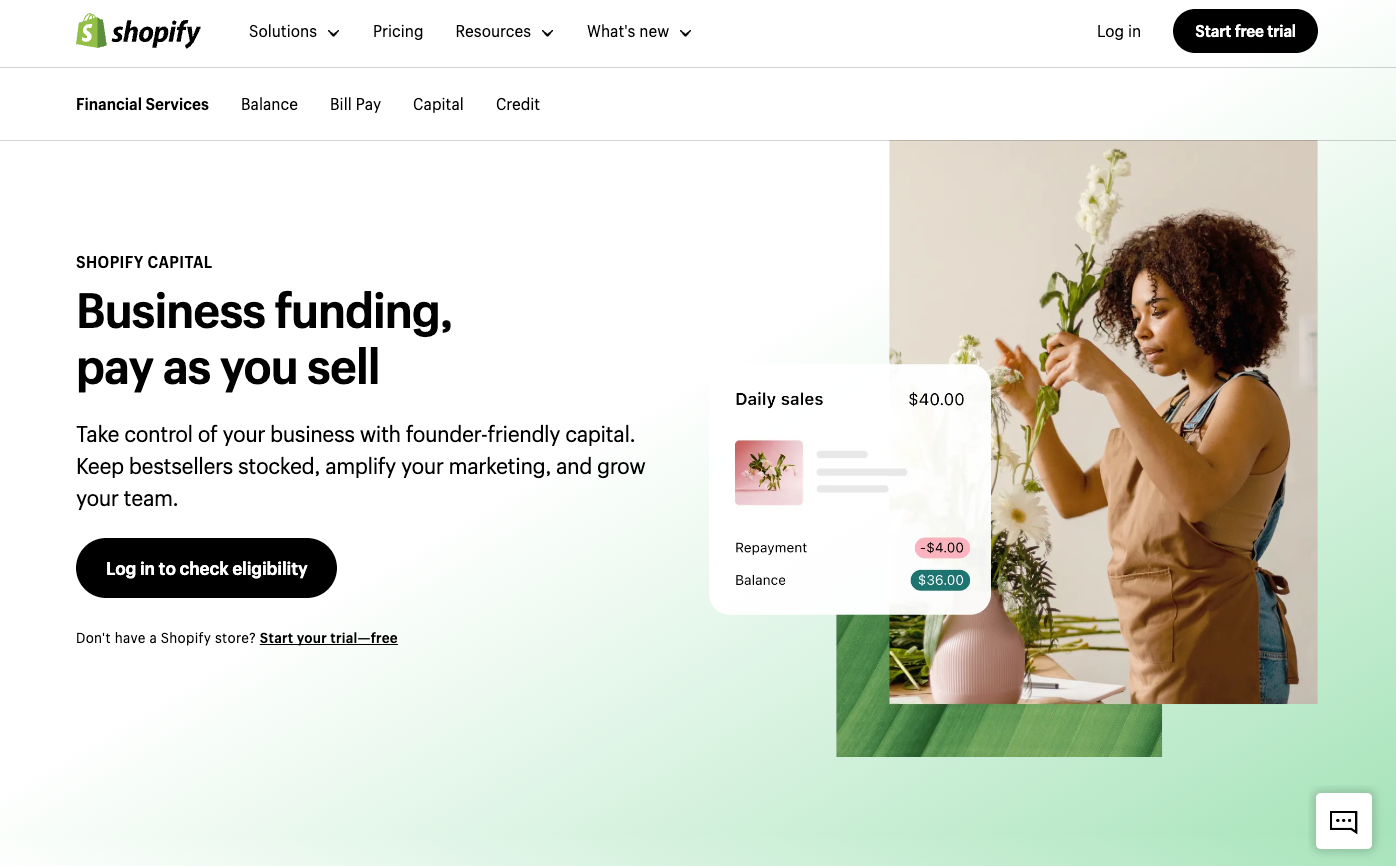

1. Shopify Capital

Shopify Capital is a financing program that offers retailers merchant cash advances. If eligible, you’ll receive a lump sum of cash for a fixed borrowing cost. The factor rate depends on your risk profile.

You can’t directly apply for a merchant cash advance. Instead, Shopify will notify you if you are eligible for funding. If you choose to apply, Shopify will then review your request and get back to you with a response within two or three business days.

Factor rates: Depends on risk profile.

2. Rapid Finance

Rapid Finance is a merchant cash advance option for small businesses owners with low credit, as this company takes into consideration a business’s full financial picture. You need three months of bank and credit card processing statements and a minimum credit score of 550. Some businesses find Rapid Finance to be expensive, but it is easy to get started and can get you money within 24 hours.

Advance amounts: From $5,000 to $500,000.

3. Reliant Funding

Reliant Funding offers MCAs up to $400,000, with factor rates based on your business qualifications.

Reliant Funding has one of the fastest application processes, with approvals within hours and next-day funding.

To qualify, you must have at least six months in business, at $60,000 in revenue annually, and a minimum 525 credit score.

Advance amounts: Up to $400,000.

Factor rates: Varies.

Is a merchant cash advance right for your business?

A merchant cash advance can be an accessible short-term funding option for your business. With fast funding and flexible payment terms, an MCA can give your store a head start—or help you grow faster, so you can set yourself apart from the competition.

Read more

- Merchant Account: Benefits, Types, and How to Open One

- Vision Board for Business: Use This Creative Tool to Accomplish Your New Year’s Resolutions

- 5 Ways Retailers Can Generate Revenue Outside of Business Hours

- Cutting Costs: 14 Ideas to Lower Retail Expenses Without Killing Product Quality

- Shoplifting: Why People Steal and How Retailers Can Prevent It

- What Is Gross Sales and How Do I Calculate It?

- What Are Net Sales and How Do I Calculate Them?

Merchant cash advance FAQ

What is a merchant cash advance used for?

A merchant cash advance is a type of financing that provides an upfront lump sum to a business in exchange for an agreed-upon percentage of future credit card and/or debit card sales. It can be used for a variety of operating expenses such as buying new equipment, expanding your business with a second location, and covering short-term cash flow needs.

What is the difference between a loan and a merchant cash advance?

The main difference between a loan and a merchant cash advance is the repayment structure. Loans are typically repaid in fixed monthly payments over a set period of time, while a merchant cash advance is usually paid back through a percentage of the borrower’s daily credit or debit card sales.